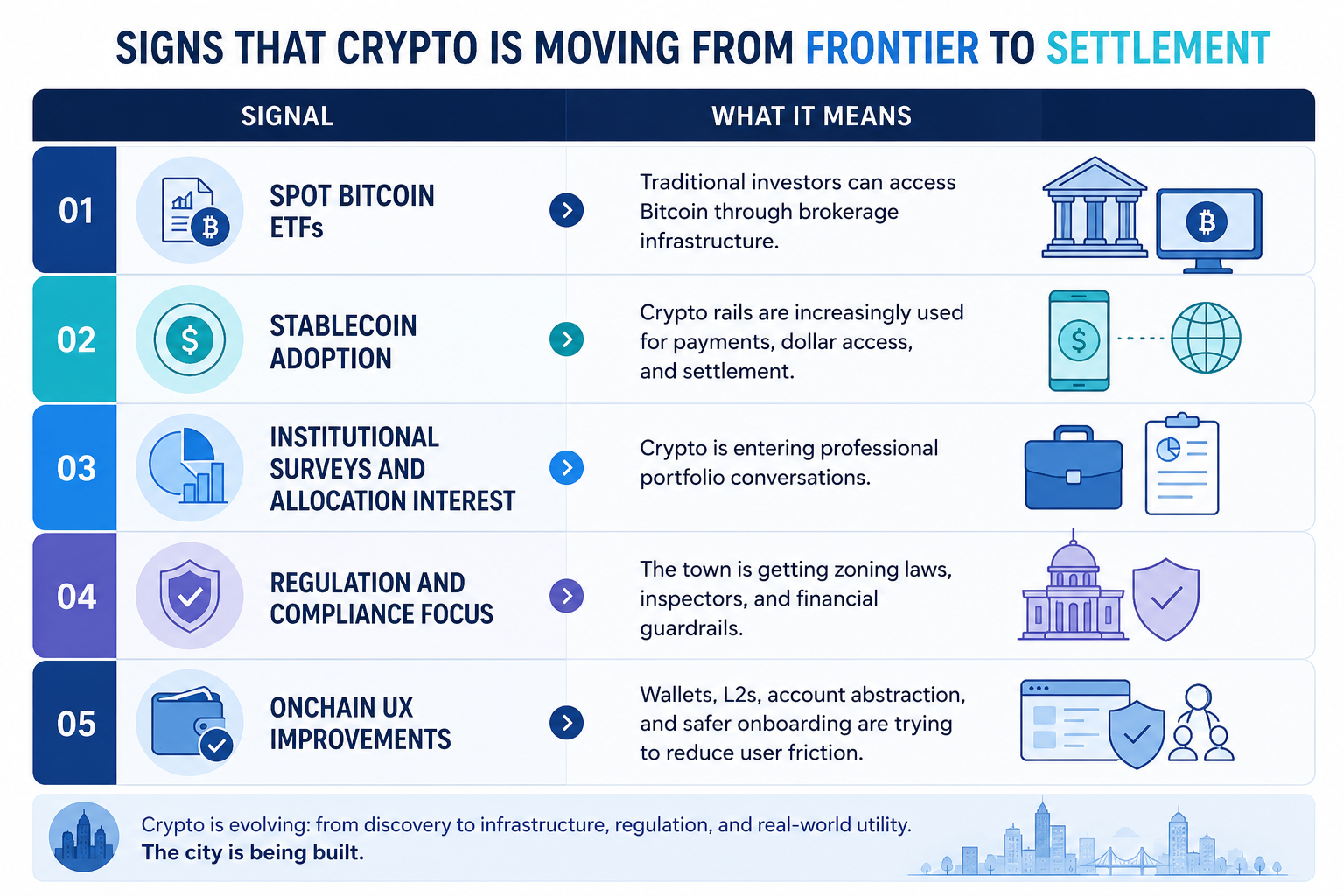

> The people who discover a frontier are rarely the same people who settle, regulate, build, insure, and eventually turn it into a functioning city. Bitcoin’s first users were not trying to build a mainstream financial product. They were reacting to distrust in banks, monetary debasement, surveillance, and centralized control. The Bitcoin whitepaper was published on October 31, 2008, proposing peer-to-peer electronic cash without reliance on a financial institution. But the crypto market today is no longer only a cypherpunk frontier. Since the 2024 approval of U.S. spot Bitcoin ETFs, crypto also became an institutional-access product inside traditional brokerage and portfolio infrastructure. Stablecoins, ETFs, tokenization, payments, and onchain finance now represent a much broader adoption curve than early Bitcoin culture. *Crypto was discovered by ideological outsiders, populated by speculators, stress-tested by survivors, and is now being established by institutions, builders, and utility-driven users. The question is whether the next wave will be trained — or exposed tourists.* --- ## The Discoverers: Cypherpunks, Skeptics of the System, and Monetary Rebels **Epoch**: 2008–2012 **User psychology**: Distrust, ideology, experimentation, sovereignty. This first group did not enter crypto because of price targets, meme coins, yield farms, or ETFs. They came because Bitcoin represented a response to broken trust. The *2008 financial crisis *created the fertile psychological ground for a system that did not require banks, central intermediaries, or permissioned settlement. These users were the discoverers of the town. They were not optimizing for convenience. They were exploring the edges of *cryptography, money, privacy, and self-sovereignty.* **Mindset:** “Could money exist outside the state and banking system?” **Blind spot:** They underestimated how difficult self-custody, key management, and mainstream usability would be for normal users. --- ## The First Settlers and Prospectors: Miners, Early Holders, and Bitcoin Believers **Epoch**: 2013–2016 **User psychology**: Conviction, curiosity, asymmetric opportunity. This wave began to treat Bitcoin less like an experiment and more like an ***asset***. Early miners, holders, exchanges, wallet providers, and infrastructure operators emerged. They were still close to the original ideology, but the market psychology was changing. The town now had roads, early shops, and maps. But it was still dangerous. Exchanges failed. Wallets were lost. Hacks were common. Regulatory understanding or clarity was absent. **Mindset:** “This thing might survive. If it survives, it could matter.” **Blind spot:** They often confused technical conviction with operational safety. Believing in Bitcoin did not automatically mean knowing how to protect private keys, manage exchange risk, or survive volatility. --- ## The Gold Rush: ICO Traders, Retail Speculators, and Narrative Chasers **Epoch**: 2017–2019 **User psychology**: Greed, urgency, social proof, fear of missing out. This is when the town became a gold rush. The *ICO boom* brought a new type of user: *less ideological, more speculative*. Many did not deeply care about decentralization. They cared about early access, token multiples, and getting in before the crowd. The psychology shifted from “Can this system change money?” to “Can this token make me rich?” This was the arrival of the merchants, gamblers, and tourists. Some real builders emerged, but so did scams, vaporware, and unsustainable promises. **Mindset:** “Every new token could be the next Bitcoin.” **Blind spot:** They underestimated incentive design, token unlocks, insider allocations, regulatory risk, and the difference between a protocol and a pitch deck. --- **The Onchain Natives: DeFi, NFTs, DAOs, Memecoins, and Reflexive Communities** **Epoch**: 2020–2023 **User psychology**: Experimentation, identity, status, financial engineering, community belonging. This wave did not just buy crypto. They used it. They swapped on DEXs, farmed yield, minted NFTs, joined DAOs, bridged assets, signed wallet approvals, and lived inside Discord, Telegram, Farcaster, and X. This was when crypto became a place, not just an asset. But the psychological profile changed again. Users were no longer only investors. They were participants in financial games, social clubs, status markets, and reflexive communities. **Mindset:** “I am not just buying crypto; I am participating in a new internet economy.” **Blind spot:** They underestimated smart contract risk, wallet-draining approvals, bridge risk, liquidation risk, social engineering, and the emotional danger of confusing community energy with durable value. The 2022–2023 crash period then separated tourists from survivors. After Terra, Celsius, FTX, NFT collapses, and DeFi exploits, many users learned that crypto does not forgive poor operational discipline. Avoid the hype and be part of a community that prioritizes both safety and process. Get our [FREE Crypto Safety Kit.](https://cryptostoicmedia.com/)[](https://cryptostoicmedia.com/) --- **The New Settlers: Institutions, Stablecoin Users, Builders, and Risk-Aware Mainstream Entrants** **Epoch**: 2024–present **User psychology**: Legitimacy, utility, compliance, portfolio access, caution, convenience. This is where we are now. Crypto is no longer only being discovered. It is being established. People will begin to benefit from crypto without knowing its running in the backend.  - Coinbase’s 2025 institutional survey reported growing institutional allocation interest, with more than three-quarters of surveyed institutional investors expecting to increase digital asset allocations in 2025. - TRM Labs also reported that stablecoin usage became a major part of global crypto adoption, with stablecoin volume surpassing $4 trillion in the first half of 2025. - Visa’s onchain analytics work also reflects the growing need to separate real stablecoin settlement activity from noisy blockchain transactions. This means the new user is different. They may not care about Austrian economics, cypherpunk mentality, or DeFi governance. Their access maybe through: - a Bitcoin ETF, - a stablecoin payment, - a crypto payroll product, - a tokenized treasury fund, - a wallet app, - a remittance corridor, - or a brand-led consumer experience. **Mindset:** “I don’t need crypto to be my identity. I need it to solve a problem, preserve optionality, or give me exposure.” **Blind spot:** They may trust the interface too much. They may assume crypto works like banking, where mistakes can be reversed and customer support can recover funds. That is dangerous. --- ## The Missing Wave: AI Agents as Crypto’s Largest Future User Base There is one category of crypto user that most adoption frameworks still underweight: **AI agents.** If the first crypto users were monetary rebels, miners, traders, builders, institutions, and stablecoin users, the next wave may be autonomous software agents that need to transact, pay, verify, subscribe, negotiate, and settle value on behalf of humans or businesses. AI agents are not “users” in the traditional sense. They need functional rails. They need programmable money. They need access to APIs, data, compute, storage, marketplaces, identity systems, and payment channels. Traditional payment systems were built around human approval, bank accounts, cards, and customer workflows. AI agents, by contrast, operate continuously, across platforms, at machine speed, and with delegated authority. That is why crypto rails are structurally attractive for agentic commerce. -** Stablecoins** give agents a programmable settlement asset. - **Smart contracts** provide rules for escrow, permissions, and conditional execution. - Onchain records offer auditability. - **Wallet infrastructure** enables custody and transfer. - **Identity systems** may help agents prove authorization and track behavior over time. This shift is already visible. Coinbase introduced *x402* as an internet-native payment protocol for APIs and agents to make instant stablecoin payments. Google has also explored an *Agent Payments Protocol* to enable secure agent-driven transactions across platforms. These are early signals that agentic payments are moving into real infrastructure. * The caveat: AI agents do possess emotions. But their creators do.* *Businesses* will ask: “What can software handle without adding headcount?” *Developers* will ask: “How can agents discover services, pay for tools, and complete workflows autonomously?” *Users* will ask: “Can my agent execute tasks safely on my behalf?” This is a powerful adoption driver, but introduces new risks. AI agents introduce automated mistakes at scale. A human can make one error. An agent can repeat that error across systems before intervention is possible. Research on agentic payment systems highlights concerns around *prompt injection, weak intent binding, privacy leakage, and authorization abuse. * The future agent wallet cannot simply mirror a human wallet. It will need: - policy controls, - spending limits, - approval layers, - identity checks, and - clear override mechanisms. The key question will not be whether an agent can pay, but whether it can operate within a safe and controlled environment. In the town metaphor, AI agents are not tourists or speculators. They are automated workers who may become the invisible labor force of the crypto economy. Users may not even realize they are using crypto. They will simply delegate tasks, and agents will execute them using programmable financial infrastructure. --- ## Where We Are in the Journey The discoverers found the town. The builders laid the roads. The institutions brought capital. The mainstream users brought legitimacy. But AI agents may bring the continuous activity that turns the town into a functioning economy. The opportunity is large. So is the responsibility to build it safely. The next wave of crypto users will not need more hype. They will need maps, rules, checklists, and safety habits. Because discovering the town was one achievement. Learning how to live there safely is the next milestone. Get our FREE [Crypto Safety Kit](https://cryptostoicmedia.com/)to stay protected from Crypto Scams and Frauds.